Oracle Corporation (ORCL) provides computer hardware, products, and services, as well as enterprise software. The company is actively working to shift the complexity of Information Technology out of the enterprise environment by engineering and distributing hardware and software that are able to work together in harmony. Oracle has obtained over 400,000 customers across more than 145 countries around the world by simplifying IT. The company's main focus is to enable other enterprises to continue to grow and innovate without having to worry about the complexity of their hardware and software, with their slogan being, "Hardware and Software, Engineered to Work Together". Oracle Corporation is organized into three different businesses: Software, Hardware Systems, and Services.

The Software business itself is actually separated into two segments itself: New Software Licenses, and Software License Updates and Product Support. The New Software Licenses segment, as the name implies, focuses primarily on the licensing (selling) of their various software products that are designed to perform a multitude of different functions. The Software License Updates and Product Support segment deals with updating client's software with patches and upgrades, and offering product support.

Oracle's Hardware Systems operation consists of two segments as well: Hardware Systems Products, and Hardware Systems Support. Similar to the organization of the Software operation of Oracle's business, the Hardware Systems Products distributes its products, which include storage products, networking components, operating systems, and others. The hardware that Oracle creates is designed to work in customer environments that include either other Oracle, or non-Oracle hardware or software components. Similar to the support available for the corporation's software side of things, the Hardware Systems Support segment is re! sponsible for providing customers with any updates necessary for software components that are necessary for the operations of the company's hardware. This segment also includes repairs, maintenance, and technical support.

The Services business is broken down into three different segments: Consulting, Cloud Services, and Education. While the Consulting segment deals with initial product implementation and ongoing product enhancements and integration, the Education segment provides training to customers and even offers a certification program that enables individuals to become certified database administrators, consultants, implementers, and others. The Cloud Services Segment provides software and hardware management and maintenance services for customers in regards to the company's cloud products.

Oracle has so much to offer to all types of enterprises. From business and financial management products, to industry specific applications software, Oracle has you covered. The company is so driven to provide your company with the total technical experience that they even have their own operating system, Oracle Solaris, which is known for its scalability and originating many innovative features.

Company History

Oracle Corporation was founded in 1977 by Larry Ellison, Bob Miner, and Ed Oates.

The company has a pretty massive history list with an abundance of acquisitions, just as most major corporations do, but here is some of the recent history:

2010: Oracle launched its "Oracle Enterprise Manager Ops Center," which is a data center automation tool that simplifies discovery and management of physical and virtualized assets. This same year, Oracle's Mexico Development Center begins operations in Mexico. Also in 2010, Oracle was indicted by the U.S. Justice Department for fraud, stating that the company failed to provide the U.S. Government with the same discounts on its software that it offered to its commercial customers (Oracle was required to do so). The lawsuit ! stated th! at Oracle overcharged the government on a contract that ran from 1998 to 2006. This issue was settled in 2012 for almost $200 million. On the other hand, near the end of 2010 Oracle Corporation won a nearly $1.3 billion lawsuit against a European software company named SAP. SAP was accused, and eventually admitted to the acts, of massive illegal downloads of Oracle's software in attempts to take customers away from Oracle.

2013: Oracle Corporation announced an agreement that it has made with Paradox Engineering to work on solutions in the smart city market. Oracle also announced recently that new in-memory applications for Oracle JD Edwards EnterpriseOne, Oracle PeopleSoft, Oracle Siebel, Oracle E-Business Suite, and Oracle Hyperion. They claim that their critical applications are now running 10-20x faster than before.

Oracle has acquired an average of more than 9 companies a year over the last eight years (including 2013). They have been busy. Here are some of the more notable acquisitions that Oracle has made over the last few years:

Acme Packet, a company in the business of providing networking hardware for telecommunications service providers, in February of 2013 for $2.1 billion.

Taleo, a company focused on talent management software, for $1.9 billion in February of 2012.

Sun Microsystems, which focuses on computer servers, storage, networks, Java, MySQL, database, software, and services, in January of 2010 for $7.4 billion.

Financial Strength

Oracle is the third largest software maker by revenue, behind only Microsoft (MSFT) and IBM (IBM). Oracle also has a higher Gross Margin percentage (81.35%) than IBM and MSFT, and a higher Operating Margin (39.28%). The company also has a higher Price to Sales ratio (4.11x) than its two largest competitors.

Over the past year Oracle has also been pushing its software offerings more towards SaaS (Software as a Service) solutions, which is being driven by customer demand. Oracle has been consuming smaller compan! ies left ! and right. With recent acquisitions of RightNow, Taleo, and Eloqua, Oracle's SaaS products should expand greatly.

Oracle also currently has a Return on Equity of 25.52%, which implies that the company is able to reinvest its earnings better than roughly 92% of its industry competitors. This is nothing new either, Oracle has had a ROE of over 20% since at least 2004 (except for 2010, which was 19.9%).

Recent growth in sales has been hampered by the hardware segment's revenue declining. The hardware segment also puts pressure on the operating margins of the company as well. This doesn't concern me much because the software segment of the company contributes to a much larger portion of sales than the hardware segment, and is also growing at a much faster rate. This should help revenue growth rates and operating margin rates increase over time.

Oracle has been doing quite a bit of stock repurchases as well. From May of 2004 to May of 2013 the company has averaged roughly $2.5 billion in share repurchases annually. In fiscal year 2012 Oracle spent $5.1 billion on stock repurchases, and almost $9.5 billion for fiscal year 2013. In June of 2013, Oracle's Board of Directors approved an expansion of the company's stock repurchase program by an additional $12.0 billion. The repurchase program does not have an expiration date, and the company stated that the pace of their stock repurchases will depend on various factors such as the company's working capital needs, cash needs for dividend payments and acquisitions, debt repayment obligations, and economic and market conditions. Oracle currently has almost enough money in cash ($39 billion) to pay off all of their short and long term liabilities ($42.8 billion).

Management

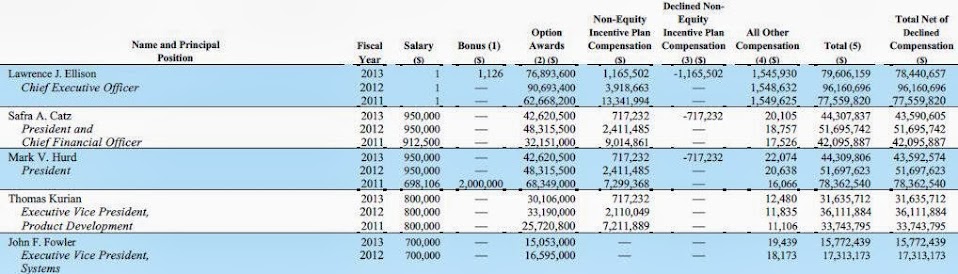

Oracle's management gets paid a lot. And when I mean a lot, I mean that the company's CEO, Larry Ellison (who also founded the company), is one of the highest paid CEO's in the country, raking in over $96 million in 2012. The fact that Mr. Ellison no! t only fo! unded the company in 1977, but is also still the corporation's Chief Executive Officer means a lot to me. Here is the summary of executive compensation:

[ Enlarge Image ]

[ Enlarge Image ]

Valuation

Oracle powers the top 10 SaaS (Software as a Service - a software delivery model in which software and data are centrally located on the cloud) providers, thousands of SaaS applications, and many of the world's private clouds. Cloud computing has seen some pretty serious growth in recent years - even the Department of Defense is hopping on board. It seems like Oracle is in the news almost daily with some sort of new announcement of enhancements or innovation to their product line. For instance, the company recently announced that it is expanding the Oracle Cloud with new services giving customers access to the world's leading database and Java application server in the cloud. These services will give customers full administrative control and managed service options.

451 Research released a study that contained several key facts concerning cloud computing growth. According to them, 69% of enterprises who have separate budgets for cloud computing are predicting to spend more this year, and in 2014, for this service. They also projected that the worldwide cloud computing market will grow at a 36% compound annual growth rate (CAGR) through 2016. This would make the market reach $19.5 billion by 2016.

Using the conventional P/E method, if we subtract the $39 billion in cash that Oracle has from the $155 billion market cap, we see that the company's operations can be purchased for $116 billion. Because Oracle has a net income of $11 billion (TTM), the company is actually trading at a P/E of 10.54 as opposed to the current 14.46. Oracle also has an estimated Forward P/E (1 year) of 10.65.

Let's take a look at using a version of the Discounted Cash Flow m! ethod (DC! F) to valuate the share price. I will use the most recent Earnings Per Share of 2.32, an 18.9% growth rate over the next 10 years (which is the average EPS growth rate of the past 10 years), a Terminal Growth Rate of 2% (average inflation rate for 2013 so far), with 10 years of Terminal Growth at a Discount Rate of 12% to be safe. That leaves us with a Fair Value of $58.85 and a 42% Margin of Safety. That's a healthy margin.

We can also look at the Peter Lynch value, which is currently at $38.81, and view the corresponding chart:

End Notes

Disclosure: No current position held at the time of writing.

Disclaimer: The opinions and ideas in this article are for informational and educational purposes only. They are not a recommendation to buy or sell any stock at any given time. As always, it is imperative for each individual investor to do their own due diligence and perform their own research on any and all stocks before making an investment decision.

No comments:

Post a Comment