As regular Growth Stock Wire readers know, I've been predicting a big drop in the benchmark West Texas Intermediate Crude (WTIC) price... I figured soaring U.S. oil production coupled with lower demand for oil products would drop the oil price down as low as $70 a barrel.

Since January 2011, WTIC has averaged $94 per barrel. It bottomed at $78 last June... That's about 10% from my estimate. But it didn't stay there long. Today, it's back up to $97. What's happening?

Exports.

Officially, it's illegal to export oil from the U.S. These rules were put in place in the 1970s, when crude was scarce. Even though things have changed dramatically, the laws stand.

That should leave a huge "captive" supply of crude here in the U.S.

But some energy companies have discovered a "loophole." While it's illegal to export oil... it's not illegal to export the products you can refine from it.

Our exports of "finished" oil products (gasoline, diesel, and jet fuel) have nearly quadrupled since 2005. They're at all-time highs.

You see, for the last 18 months, foreign oil (Brent crude) has traded at a 20% premium to WTIC. So there is huge international demand for products made from the "cheap" American oil. We're shipping product to South America, Africa, Asia, and Europe.

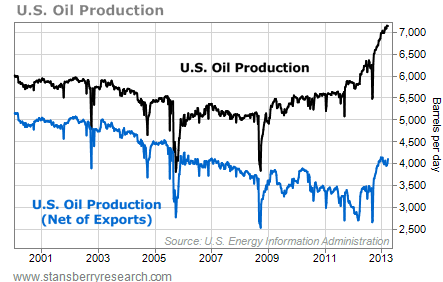

It's having a dramatic effect on our actual oil supply... Take a look at this chart...

The black line represents total U.S. production. By itself, it would spell that epic drop in oil prices. But the blue line is U.S. production, minus the crude that's being refined for export. It's ramping up... but not nearly as high as the blue line.

Exports now equal a huge 41% of U.S. oil production. They're helping keep the oil supply under control. While a capacity pinch at the refiners could push oil prices down, I no longer believe oil will crash below $70.

That's great news for oil investors right now. We can buy oil and gas producers without the fear of an oil price cliff looming in the near future. And right now, there are stocks trading as though oil prices are headed lower...

To measure value in oil producers, I like to use enterprise value (which is the market cap plus debt minus cash) divided by earnings (before interest, taxes, depreciation, and amortization). This "EV/EBITDA" measure gives us a good "big picture" view of a company.

The average EV/EBITDA in the industry right now is 13.4. But top names like Marathon, Apache, and Newfield have EV/EBITDAs under four.

I'm bargain-hunting in this sector right now. I suggest you do the same.

My top "energy income" investments are royalty trusts. They simply collect cash from oil and gas wells drilled on their lands and distribute it to owners.

They are passive, low-risk investments that, if bought at the right time, can provide commodity investors with double-digit yields... and you don't have to depend on commodity prices rising.

As I've been showing you over the last year, low natural gas prices have depressed their distributions. That's no problem if you buy at a low price...

But now, there's another wrinkle to the story.

San Juan Basin Trust (NYSE: SJT) is one of the top names in the sector. It generates royalties from wells drilled by ConocoPhillips in the San Juan Basin (in Colorado and New Mexico). But with natural gas prices at today's depressed levels, you just can't make money drilling new wells there.

So Conoco said it was going to stop drilling wells. And that's a major problem for SJT.

SJT's wells are old and in decline. It needs new wells to generate more revenue. If it doesn't get those wells, its distributions are going to fall... even if natural gas prices hold steady.

If you jumped back into San Juan Basin, I suggest getting out. Shares of this trust are going lower.

And I expect many operators to follow ConocoPhillips' lead... That's going to hurt folks who specialize in drilling natural gas wells. If you own shares of drilling companies, tighten your trailing stops.

– Matt Badiali

No comments:

Post a Comment